California Home Financing Options for 2025: What Buyers in Orange County Should Know

By Bryan Suarez, Local Real Estate Agent Serving Moulton Ranch, Mission Viejo, Lake Forest, Rancho Santa Margarita, Aliso Viejo, Laguna Niguel, Castille and Surrounding Areas

Buying a home in California — especially here in South Orange County — can feel overwhelming. The market is competitive, the prices are high, and mortgage rates are a major factor. But there are multiple financing paths you can take. In this post, I’ll break them down in clear, practical terms — so you can pick what fits your goals and budget.

1. Conventional Loans: The “standard” option

This is what most people think of first. These are mortgages not guaranteed by the government (but often conform to Fannie Mae / Freddie Mac rules).

Key points:

-

Down payments typically 3% to 20%, depending on your credit and lender.

-

If you put down less than 20%, you’ll usually pay private mortgage insurance (PMI) until you reach that equity threshold.

-

Good credit scores (often 700+) and lower debt ratios help you qualify for better rates and terms.

-

Flexible: can use for primary homes, second homes, or investment properties (though qualification standards tighten for investment uses).

In Orange County high-cost markets, you may hit conforming loan limits, so sometimes you’ll need a jumbo loan (more on that later).

2. Government-backed / insured loans: FHA, VA, and more

These are loans backed (or guaranteed) by federal agencies — useful especially when your down payment or credit is less than ideal.

FHA (Federal Housing Administration)

-

Requires as little as 3.5% down for credit scores around 580+.

-

More lenient credit requirements than conventional in many cases.

-

You’ll pay mortgage insurance (MIP), usually for the life of the loan (or long term).

-

Good option for first-time buyers or those rebuilding credit.

VA (Veterans Affairs)

-

For eligible veterans, active service members, or surviving spouses.

-

Often 0% down, no PMI, and favorable interest rates.

-

Must meet VA eligibility rules and get a VA appraisal.

-

A powerful option if you qualify.

USDA (Rural / semi-rural areas)

-

Designed for rural or less densely populated areas.

-

Some programs allow 100% financing (no down payment).

-

Income limits apply.

-

In recent years, USDA expanded rules around manufactured homes too.

3. Jumbo Loans: for high-value homes

Because many homes in California exceed standard conforming limits, a jumbo loan is often necessary.

-

Higher loan amounts (above conforming caps).

-

Typically stricter credit score, debt ratio, cash reserves requirements.

-

Slightly higher interest rates.

-

Often require 10–20% down (or more).

-

Be prepared to show stronger documentation and financials.

4. Adjustable-Rate Mortgages (ARMs) & hybrid loans

If you don’t plan to stay in the home for decades, or if you expect rates to fall, ARMs or hybrids can make sense.

-

Example: a 5/1 ARM — fixed rate for first 5 years, then adjusts annually.

-

Lower initial interest rate compared to fixed.

-

Risk: rate (and monthly payment) may increase later.

-

Strategy: use ARMs if you anticipate selling or refinancing before the reset.

5. Specialty & alternative financing paths

These are useful when your income, employment, or property type doesn’t meet traditional standards.

-

CalHFA Programs (California Housing Finance Agency): Down payment assistance, first-time buyer programs.

-

Bank-statement / self-employed loans: Use bank statements instead of pay stubs.

-

203(k) / renovation loans: Combine purchase + rehab funding into one mortgage.

-

Bridge loans: Short-term financing to “bridge” when you sell one home and buy another.

-

Hard money / private money: Short-term, asset-based loans (mostly for investors or fix-and-flip).

-

Equity-based loans / HELOCs: Using home equity for renovations, etc.

6. How to pick the right one (for OC buyers)

Here are a few decision criteria I use with my clients in South OC:

-

How long you plan to stay — If it’s long term, prefer fixed-rate conventional or FHA.

-

How much down payment you have — Limited funds may push toward FHA, CalHFA, or low-down conventional programs.

-

Your credit / debt profile — Insurance programs (FHA, VA) tend to accept more flexibility.

-

Home price vs conforming limits — If the property is expensive, you’ll likely need a jumbo loan or an alternative path.

-

Your risk tolerance — ARMs are riskier long-term if rates rise.

-

Special qualifications — If you’re a veteran, teacher, or first-time buyer, there may be unique programs you don’t want to miss.

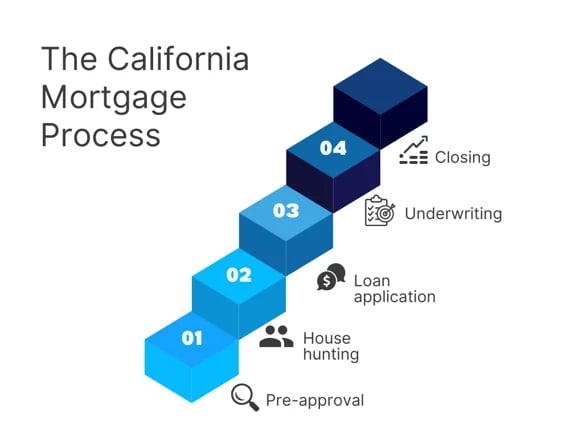

7. Steps to take NOW

-

Speak with a trusted lender and get pre-approved. If you don't have one, I have several that I can recommend.

-

Ask about all available programs (some lenders specialize in niche or state programs).

-

Understand full cost — not just interest rate, but PMI, mortgage insurance, closing fees, etc.

-

Lock in favorable rates when you can, or negotiate float-down clauses.

-

Stay in touch — market changes, rate moves, or new programs may shift your best option.

Bottom line: There is no one perfect loan — it’s about matching your unique finances, timeframe, goals, and risk tolerance. With the right guidance, even in a challenging market, you can find a financing path that makes sense for your Orange County home dream.

If you’d like me to run side-by-side scenarios for your situation (how much down payment, your credit, your ideal neighborhoods in South OC), I’d love to help. Just drop me a message and we’ll map it out together.

-Bryan

📞 (949) 522-7502

📧 [email protected]

Bryan Suarez Real Estate | Top Realtor in Mission Viejo, Orange County

You might also be interested in:

Orange County Housing Market 2025: Trends, Prices & What Buyers and Sellers Should Know

Relocating to Orange County? Your Complete Moving Guide!

Buy Before You Sell: The Smart Move for Orange County Homeowners

🏡 What Homebuyers Need to Know About Touring Agreements: A Guide from a South OC Real Estate Expert